2026 1st Quarter Market Commentary

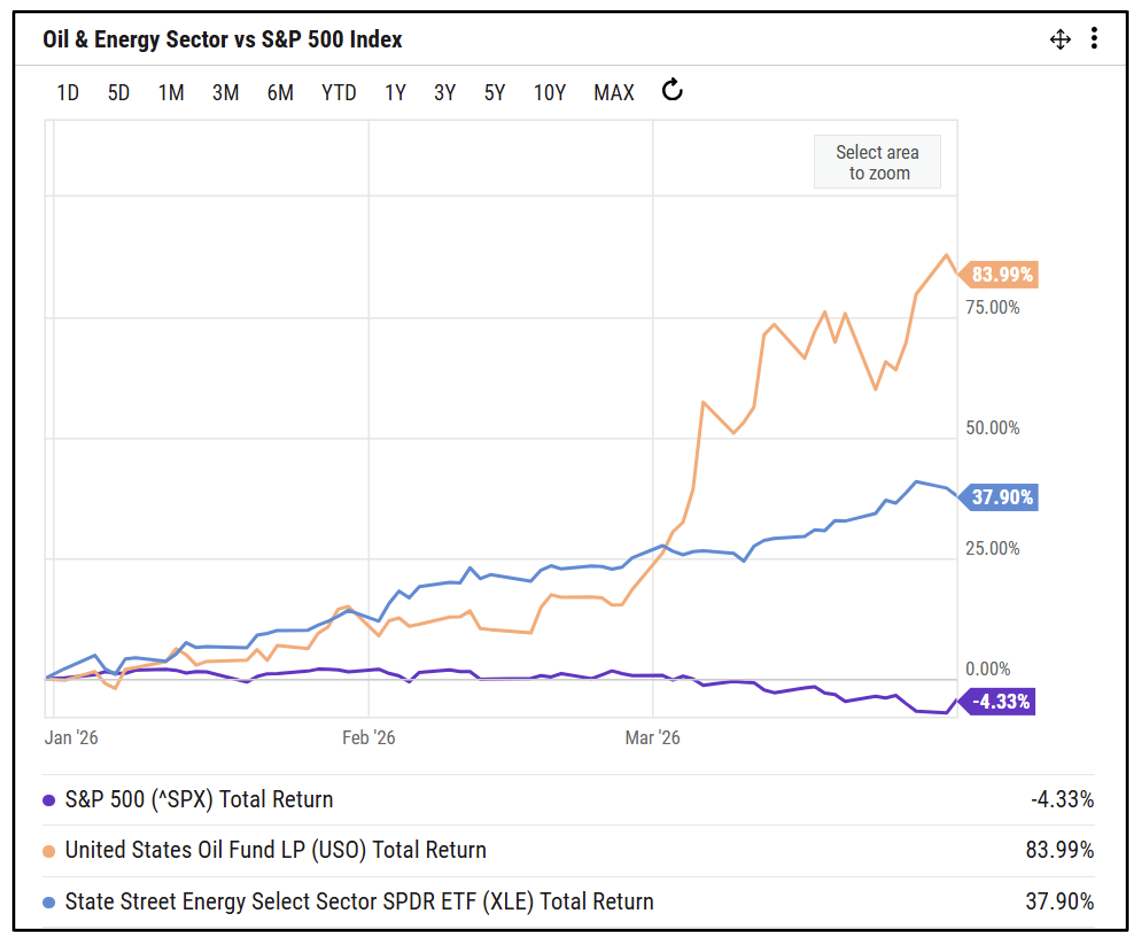

The first quarter of the year was defined by a single geopolitical event and its cascading effects across asset classes. The most interesting chart from Q1 is the price of oil. The conflict in Iran, which led to reduced shipments of oil flowing through the Strait of Hormuz, created a market “shock” (i.e., rapid escalation in global oil prices). The chart below shows both the price of oil (as measured by the ETF USO) and the S&P energy sector proxy (XLE). Oil soared by a whopping 84% during the quarter. The energy sector, whose profits tend to be highly correlated with the price of oil, also rose sharply (up 37.9%).

The problem with rising oil prices is that oil (i.e., energy) is a primary operating input in almost every business in the world. Rising energy prices are viewed as inflationary. So, they tend to reduce corporate profits and can have recessionary impacts on consumers who tend to spend less on other goods as energy becomes a larger part of consumer spending. It’s also noteworthy that this shock has had adverse impacts on the interest rate market. More specifically, current U.S. Federal Reserve Bank guidance, via their “dot plot”, points to only one rate cut through the rest of 2026 – down from the three anticipated cuts in late 2025 – as they brace for lingering inflation.

General Market Update

US Equities: The S&P 500 Index fell 4.33% during the quarter while the equal-weighted S&P 500 Index (Ticker: RSP) was up 0.61%. The tech-heavy Nasdaq Composite finished down 6.96% and the Russell 2000 small cap index was up 0.89%. On the surface these numbers aren’t too alarming but at one point during the quarter, the S&P 500 Index had a -9.8% drawdown (1/28 – 3/30) and the Nasdaq 100 had a -13.7% drawdown (1/28 – 3/30), before staging a strong rally over the last two days of the quarter. We’ve been highlighting the market concentration risk and elevated technology sector pricing for some time now. This quarter proved an opportune time to have diversified exposures to some of the “unloved” sectors and to consider exposure to “equal weighted” indices. As highlighted above, Energy tops the list of winning sectors for the quarter, but we also saw great performance from Materials (XLB) up 10.7%, Utilities (XLU) up 8.3%, Consumer Staples (XLP) up 6.1% and Industrials (XLI) up 4.6%.

International and Emerging Market Equities: International markets continued their positive momentum from 2025, despite being more impacted by rising oil costs. The Schwab International Equity ETF (SCHF) was up 2.95% for the quarter and the Schwab Emerging Markets ETF (SCHE) was up 0.6%. Europe, in general, is more dependent on importing foreign oil. After the Iran attacks, SCHF saw a -12.2% decline from February 27 through March 30. Overall, both indices have solidly outperformed the U.S. equity markets on a rolling 12-month basis.

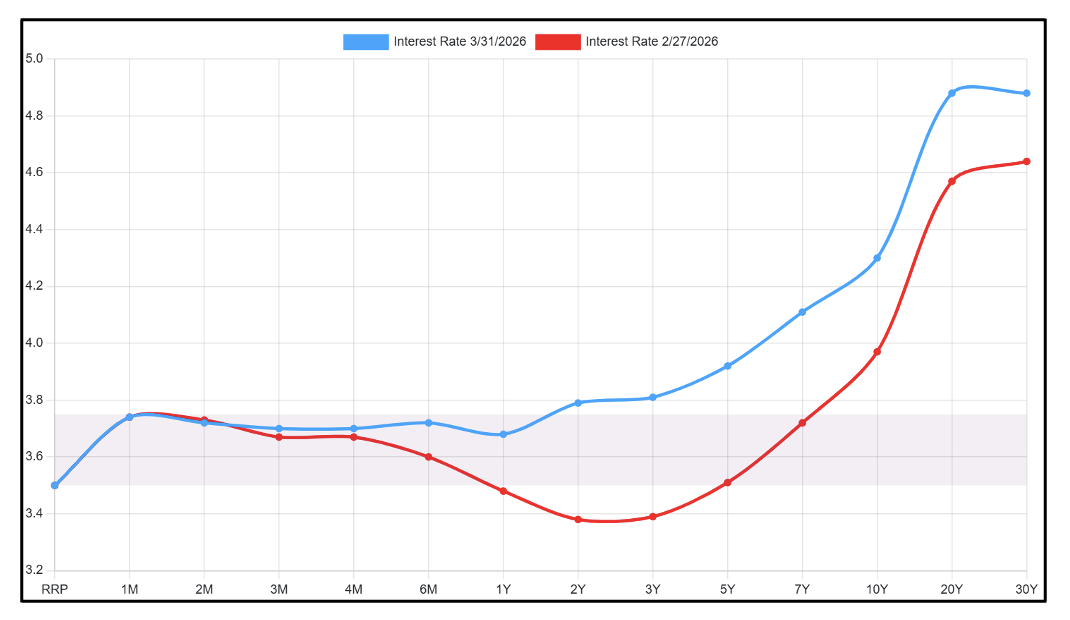

Fixed Income and Credit: As mentioned above, energy prices are a key factor in determining inflation which, in turn, drives impacts in the interest rate market. More specifically, as expectations for inflation increase, the entire “Yield Curve” shifts higher as investors demand higher returns for a given maturity date. We certainly saw this in March of 2026 as the 10-Year U.S. Treasury bond yield went from around 4.0% to 4.3% in just one month with even bigger impacts in the 2 to 7-year timeframe (see chart below).

While we have been favoring income investments with shorter maturities, we are now beginning to see increasing value in medium and long-term bonds. We will be watching closely to see if the 20-year+ U.S. Treasury bonds push back above 5% - a key milestone that has recently marked a good buying opportunity.

Pro-Inflation Investments: Precious metals finished the quarter relatively flat after peaking near the end of January and falling through February and March. Gold and Silver were not immune to the cross-asset volatility. After peaking on January 29, Gold (GLD) fell an eye-opening -21.7% through March 24 and Silver (SLV) fell -45% from January 29 through March 26. It appears that the historic run for precious metals may be paused, for now. We continue to like pro-inflationary investments as governments fail to rein in spending but many portfolios saw decreased exposure to precious metals during the quarter.

A Look Ahead

We continue to be on alert for market volatility. In the near term, the actions in Iran will continue to have material, and immediate, implications for global equity and bond markets. Given the uncertain outcome and potential for lingering impacts, investors must remain nimble. And as we’ve seen recently, any positive developments would be welcomed by the market. It’s noteworthy that while the equity markets have been relatively quiet, we’ve seen tremendous volatility in other areas (e.g., precious metals, oil/energy, interest rates and commodities to name a few). As we’ve discussed in past letters, we welcome volatility as it provides rebalancing opportunities for client portfolios.

Regarding U.S. equities, the “Mag 7” and the Technology sector were one of the hardest hit sectors during Q1 and could potentially lead the market should we see a recovery attempt in the coming months. In addition to mega-cap technology, clients will continue to see a balanced approach in portfolios. Our sense is that market participants are starting to place a premium on businesses with reasonable valuations and high cash flows.

As we look out further into the year, we see a couple of events that could continue to keep investors on edge. We have talked in the past how the stock market doesn’t like uncertainty. In the coming months the Federal Reserve will transition its leadership away from current Fed Chair, Jay Powell, to the current nominee, Kevin Warsh. It’s no secret that the current administration wants a Fed Chairman and Board full of “doves” (i.e., those who favor lower rates and easy-money conditions.)

In addition, the U.S. midterm elections will be held this Fall, causing more uncertainty leading up to it. The “Prediction Markets” (e.g., Kalshi) are now showing a 50/50 probability of the Senate being won by either party.

In our opinion, the market may very well breathe a “sigh of relief” after it gets past these two events but we could very well see heightened volatility before then, both on the upside and downside. We will continue to closely monitor portfolios and view volatility as an opportunity.

This article is for informational and educational purposes only and does not constitute financial advice. The analysis presented here is based on publicly available data and represents a general perspective. All investment decisions should be made with the guidance of a qualified financial professional and based on a thorough understanding of your personal financial situation and risk tolerance. Past performance is not a guarantee of future results. Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur.