The Use Case for “Equal Weighted” Investments

We’ve all been inundated of late with warnings of the “top-heavy” U.S. equity market. The data is clear - we have one of the most concentrated U.S. markets in history with over 35% of the market value in just 10 stocks. In this article we take a closer look at “equal-weighted” investments, where all holdings represent the same percentage of a given exchange-traded-fund (“ETF”), and how they may differ from their “cap-weighted” counterparts. Equal-weighted investments provide upside exposure but mitigate the potential volatility of being overly exposed to price fluctuations in “mega-cap” (i.e., extremely large) companies.

The U.S. Market Concentration is Stunning

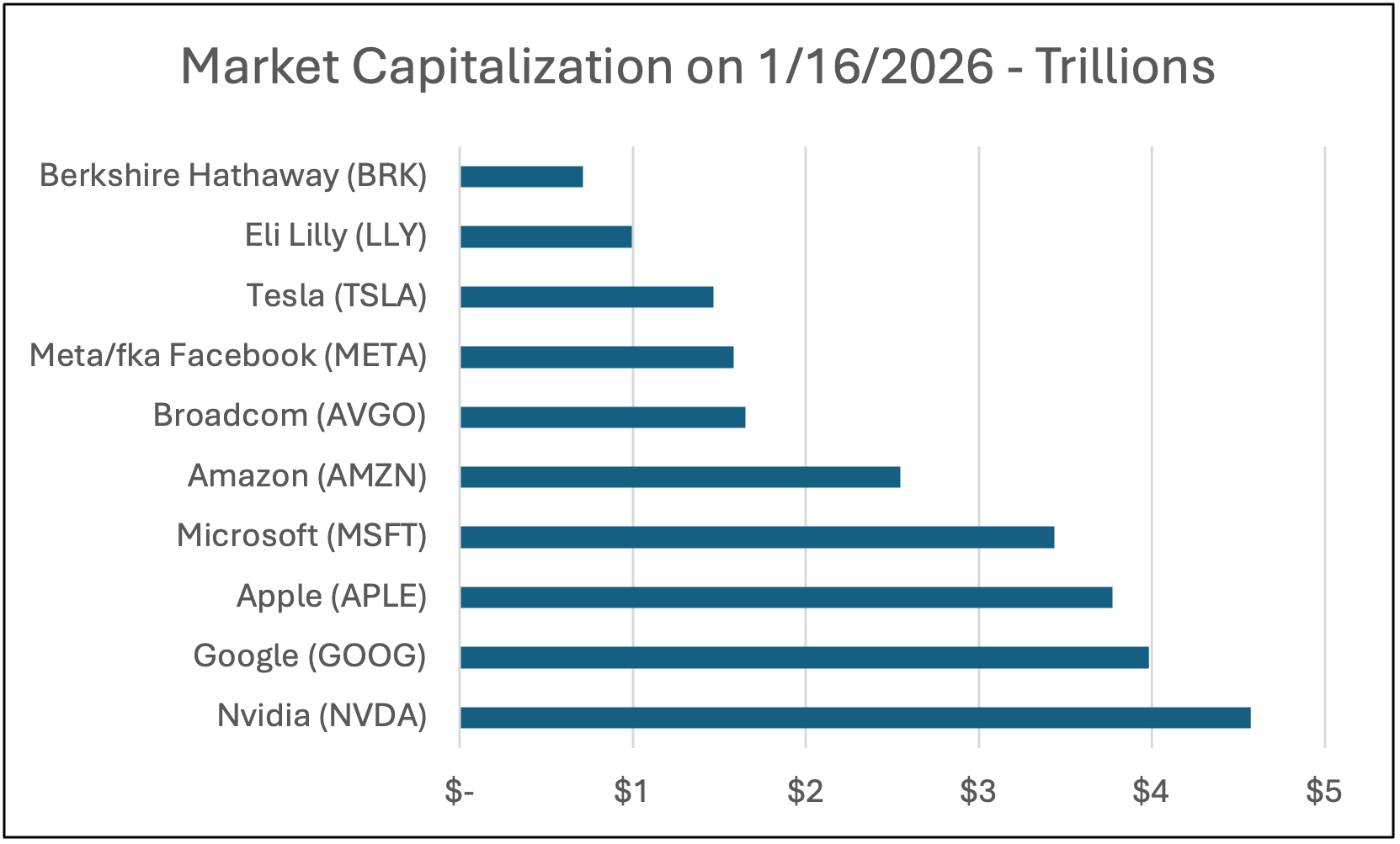

The chart below shows the size (i.e., “market capitalization”) of the “Top 10” exchange-traded U.S. companies which now represent a combined value of around $25 trillion dollars.

Source: Interactive Brokers, data as of 1/16/26

Here are a few highlights to give you a sense of the sheer scale of these companies.

· Nvidia is larger than the entire stock market of all countries in the world except for China, Japan & India.

· These 10 companies together are now worth more than what the entire U.S. equity market was worth in 2010.

· The approximate value of all ~2000 members of the Russell 2000 (small cap) Index is only around $3 trillion.

· Each of the top 8 companies is individually larger than the entire combined value of all exchange-traded U.S. equity real estate investment trusts (“REITs”) - over 190 companies with vast real estate holdings.

For those who follow Patina, you know that we have been tactically deploying into equal-weight ETFs for some time (e.g., using the equal-weighted RSP ETF alongside the cap-weighted SPY). We expect to do more of this in the year ahead in certain sectors of the market.

Equity Concentration Extends to Sectors

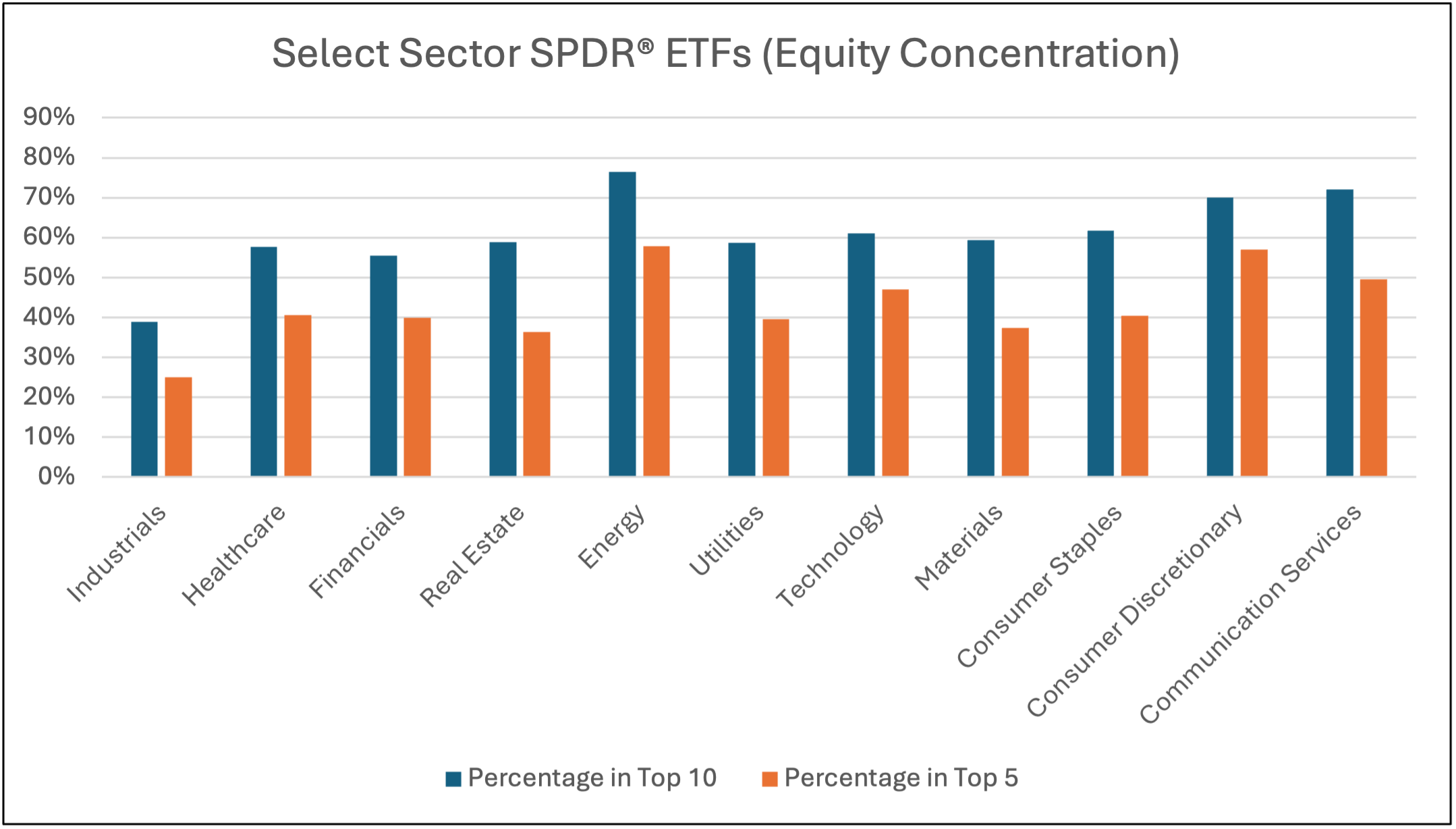

While the analysis of the ten largest U.S. stocks is eye-catching, it’s noteworthy that the market is top-heavy by other measures as well. The most widely used sector ETFs are those created by State Street (the “Select Sector SPDR® ETFs”). When one examines the equity exposures within these ETFs, it becomes clear that these ETFs suffer from the same issue as the broad indices – a (potentially unintended) dependency on a small number of companies. For example, the chart below shows the percentage of these ETFs that are in the largest holdings. While we tend to think of equity concentration as a technology-related phenomenon, the issue exists across all U.S. equity sectors. In fact, the worst culprit is Energy, where the Top 5 companies represent nearly 60% of the sector (with over 40% in just two companies – ExxonMobil & Chevron).

Source: ETFdb.com, data as of 1/16/26

The Case for Equal-Weight Tools

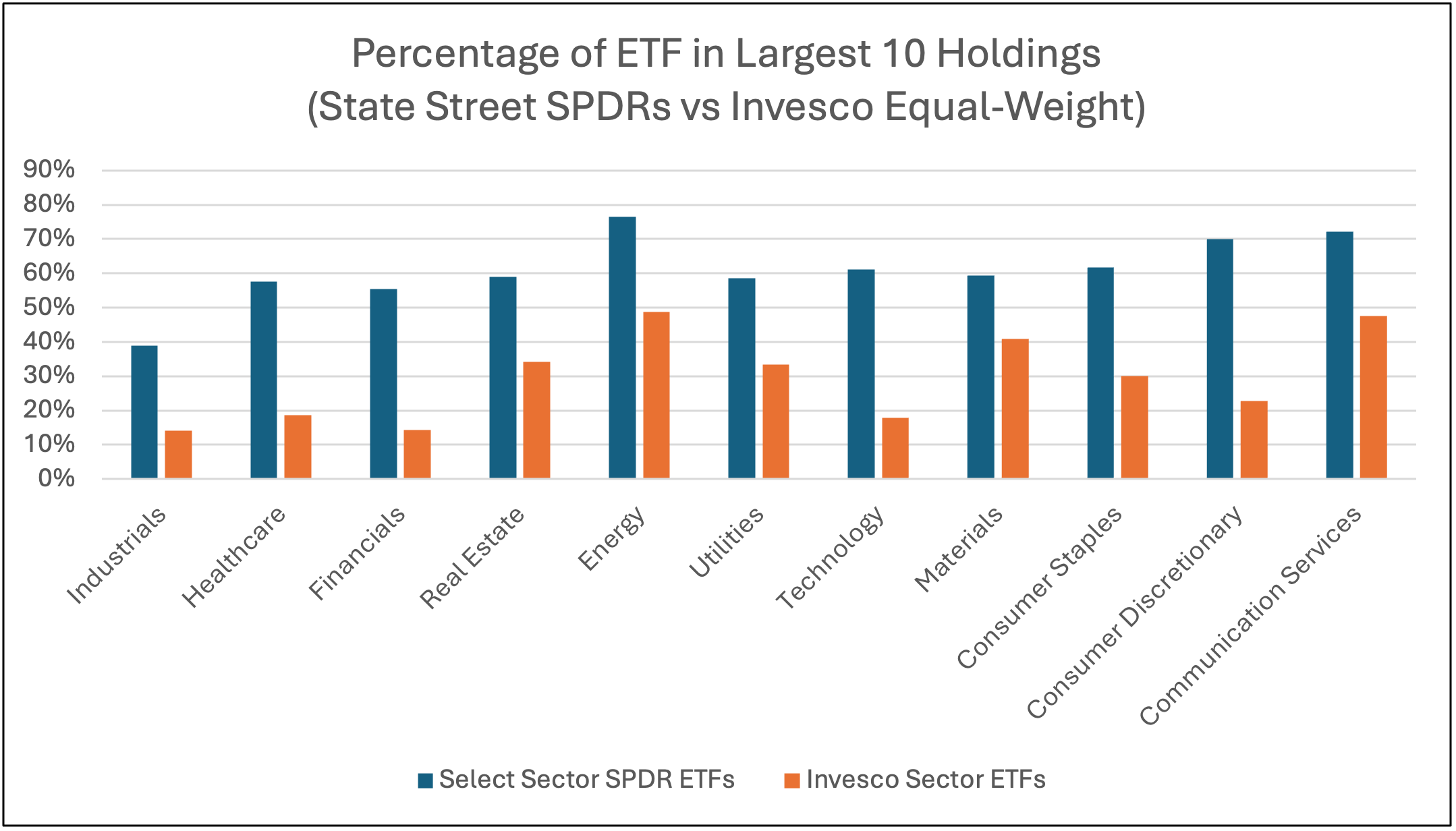

Fortunately, the ETF universe offers several tools to combat this market concentration issue. When it comes to sectors, there are ETFs that provide for a more balanced approach to gaining exposure. For example, Invesco offers a suite of sector ETFs that use an equal-weight approach. In the chart below, we compare the concentration of the ten largest holdings in the Invesco ETFs to the State Street ETFs from the chart above. It’s clear that the equal-weight Invesco ETFs greatly reduce any concentration-related risks.

Source: ETFdb.com, data as of 1/16/26

It is noteworthy and interesting that not all sectors provide the same ability to gain diversification. For example, the Invesco Healthcare ETF was able to dramatically reduce the top - 10 concentration (i.e., from 58% to 19%). However, Energy remains a challenge with a less impressive drop (i.e., from 77% to 49%).

Conclusions

In summary, U.S. equity market concentration is running at historical highs which presents inherent (concentration-related) risks. We believe risks include downside volatility as well as limited growth potential given the sheer size of the U.S. mega-caps. When seeking to gain exposure to the U.S. equity market, investors may benefit from considering tools that favor equal-weighting over cap-weighting. These benefits extend to tactical sector investing where equal-weighted tools provide a more diversified approach, providing more exposure to smaller capitalization companies within various sectors. As we move forward in 2026, Patina expects to deploy more capital into these tools in our ongoing effort to take advantage of any changes in market momentum.

This article is for informational and educational purposes only and does not constitute financial advice. The analysis presented here is based on publicly available data and represents a general perspective. All investment decisions should be made with the guidance of a qualified financial professional and based on a thorough understanding of your personal financial situation and risk tolerance. Past performance is not a guarantee of future results. Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur.