2026 2nd Quarter Market Commentary

Top Headline for Q2: Soaring Microchips Overshadow Broad-Based Rally

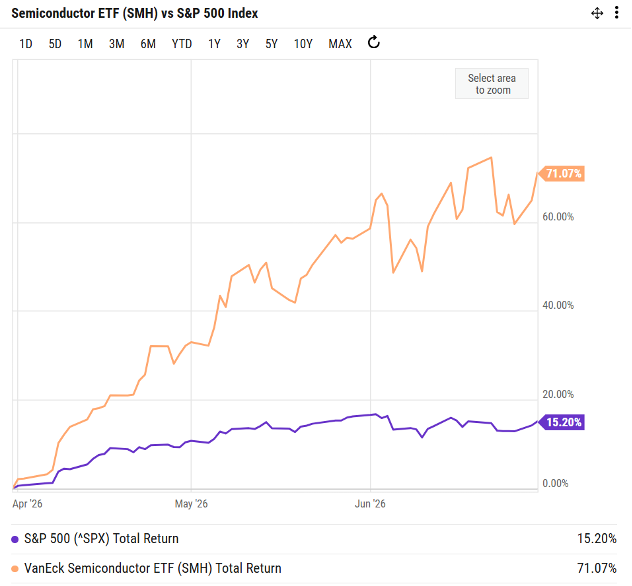

The AI trade was on full display in Q2 as microchips took center stage. As we end Q2, we now have a microchip stock (Nvidia) as the largest company in the world with two others, Broadcom and Micron, that have joined the “Trillion-Dollar Club” (i.e., market capitalizations above $1 trillion). With the latest surge, three of the 10 largest companies in the U.S. earn a majority of their revenue from microchips (wow!). The chart below shows the Semiconductor ETF (SMH) which climbed 71% for the quarter. With this surge, it is estimated that semiconductor stocks make up around 20% of the U.S. stock market capitalization.

4/1/26 - 6/30/26 performance of SMH vs S&P 500 Index

What’s overshadowed by the SMH move is that we experienced one of the best quarters ever for the S&P 500 Index, which rose 15.2% for the quarter. Q1’s drawdown ended on March 30, aiding in the timely bounce during Q2. What’s noteworthy for investors is that the move was quite broad-based – a signal that historically suggests persistence of trend. For example, 8 of the 11 S&P sectors finished up for the quarter, led by technology. Other standout performances came from industrials (XLI up 14.8%), financials (XLF up 9%), real estate (XLRE up 8.8%) and healthcare (XLV up 8.7%). As the quarter ended, we began to see some pullback in semiconductor stocks and would expect the forgotten sectors to be beneficiaries of any capital reallocation.

General Market Update

U.S. Equities: As mentioned above, the S&P 500 Index rose 15.2% during the quarter. As further evidence of the market rally being broad-based, we note that the equal-weighted S&P 500 Index (Ticker: RSP) was up 11.3%. The tech-heavy Nasdaq Composite posted a very strong quarter (up 21.6%) and the Russell 2000 small-cap index was up 21.5%. We continue to observe some of the highest levels of market concentration risk ever and, as such, are allocating to non-tech sectors and value stocks. In what we see as a healthy market rotation, June experienced a tremendous dispersion between growth and value (e.g., Vanguard's Large Cap Growth ETF (VUG) was -4.2% while Schwab's Large Cap Value ETF (SCHV) was +4.2% for the month).

International and Emerging Market Equities: International markets maintained their positive momentum for another quarter. The Schwab International Equity ETF (SCHF) was up 12.6% for the quarter and the Schwab Emerging Markets ETF (SCHE) was up 10.2%. It’s been a tremendous trailing 12-month period for both indices with SCHF up 29.7% and SCHE up 23.8% since 6/30/2025.

Fixed Income and Credit: Last quarter we highlighted how rising energy prices contributed to above-target levels of inflation. Inflation has proven to be a persistent problem – so much so that the Federal Reserve’s next move is projected to be a rate hike. The rapid change in expectations from the beginning of the year has pushed rates higher and bond prices lower. This movement is most notable in the 2 to 8-year bond range. For example, 2-year U.S. treasury yield, which many think forecast Federal Reserve actions, rose from around 3.5% to 4.25% between 12/31/2025 and 6/30/2026. While oil prices are coming down, the current (high) inflation readings along with solid employment numbers are not giving the Fed a reason to cut rates. In this environment we will generally overweight shorter duration bonds.

Pro-Inflation Investments: Despite the persistently high inflation, precious metals retreated some during the quarter. This price change is not surprising as metals have consistently served as a good long-term hedge but tend not to be correlated with inflation metrics in the short term. We continue to like pro-inflationary investments until developed nations start balancing budgets. As a reminder, any “real asset” investments may be beneficial here including commodities, industrial metals and classic sectors like real estate and basic materials.

A Look Ahead

We continue to anticipate equity market volatility as we look ahead to the second half of 2026. It’s hard to view the soaring SMH chart, and corresponding market concentration, and not think the technology sector is overdue for a pullback. Of course, it’s impossible to predict the timing, but still prudent to rebalance in the face of such moves. Given the heavy technology weighting within the S&P 500 Index, any drawdowns at the index level may look worse than what's happening in non-tech sectors.

Despite some clarity in Iran and falling energy prices, inflation expectations continue to be volatile, which leads to volatility in bond prices. Limiting bond duration is a natural strategy to combat this challenge – especially when you can still earn 3.5-4.5% on high quality short-term U.S. Treasury and corporate bonds. It’s notable that the new Federal Reserve Chairman Warsh has proven “hawkish” in early speeches, so we now expect the Federal Funds Rate to hold steady for a while.

The big potential driver in the back half of the year is, of course, the November elections. We’re skeptical that the actual election result will have a material market impact. But, the weeks leading into the election will likely cause some nervousness and uncertainty for investors, potentially leading to market volatility. We would welcome this opportunity to rebalance client accounts.